- Wealth Made Simple

- Posts

- Is it smarter to invest a bonus all at once or spread it out?

Is it smarter to invest a bonus all at once or spread it out?

Solid proof that lump sum investing often wins, but dollar-cost averaging can save you from the one mistake that ruins portfolios. Here’s how to decide.

Marcel Miu, CFA, CFP

August 24, 2025

The Windfall Dilemma

Picture this.

You just got a six-figure bonus. Or you had a huge chunk of RSUs vest.

The first feeling is excitement, but the second is anxiety.

Do you put the entire sum into the market today? Or spread it out over months to avoid regret if the market crashes?

This is the windfall dilemma. It’s not just a math problem, it’s an emotional one too.

The Data vs. Your Gut: A Framework for Your Windfall

The question: Should I invest it all at once or spread it out?

The data leans toward lump sum investing. Studies show it outperforms dollar-cost averaging across virtually all timeframes. Why? Because markets rise more often than they fall. Every day you sit in cash, you risk missing gains.

But the gut leans toward dollar-cost averaging. Because while math favors lump sum, behavior tilts you the other way. Few things feel worse than investing a big sum right before a 20% drop. That kind of regret causes panic. And panic often leads to selling, which then locks in a loss.

Vanguard research pegs the value of good behavioral coaching (investing-related) at roughly 1.5% per year. That’s not from clever stock picks. It’s from avoiding mistakes like the one outlined above. DCA is simply a built-in behavioral coach.

The Case for Lump Sum Investing: Time in the Market

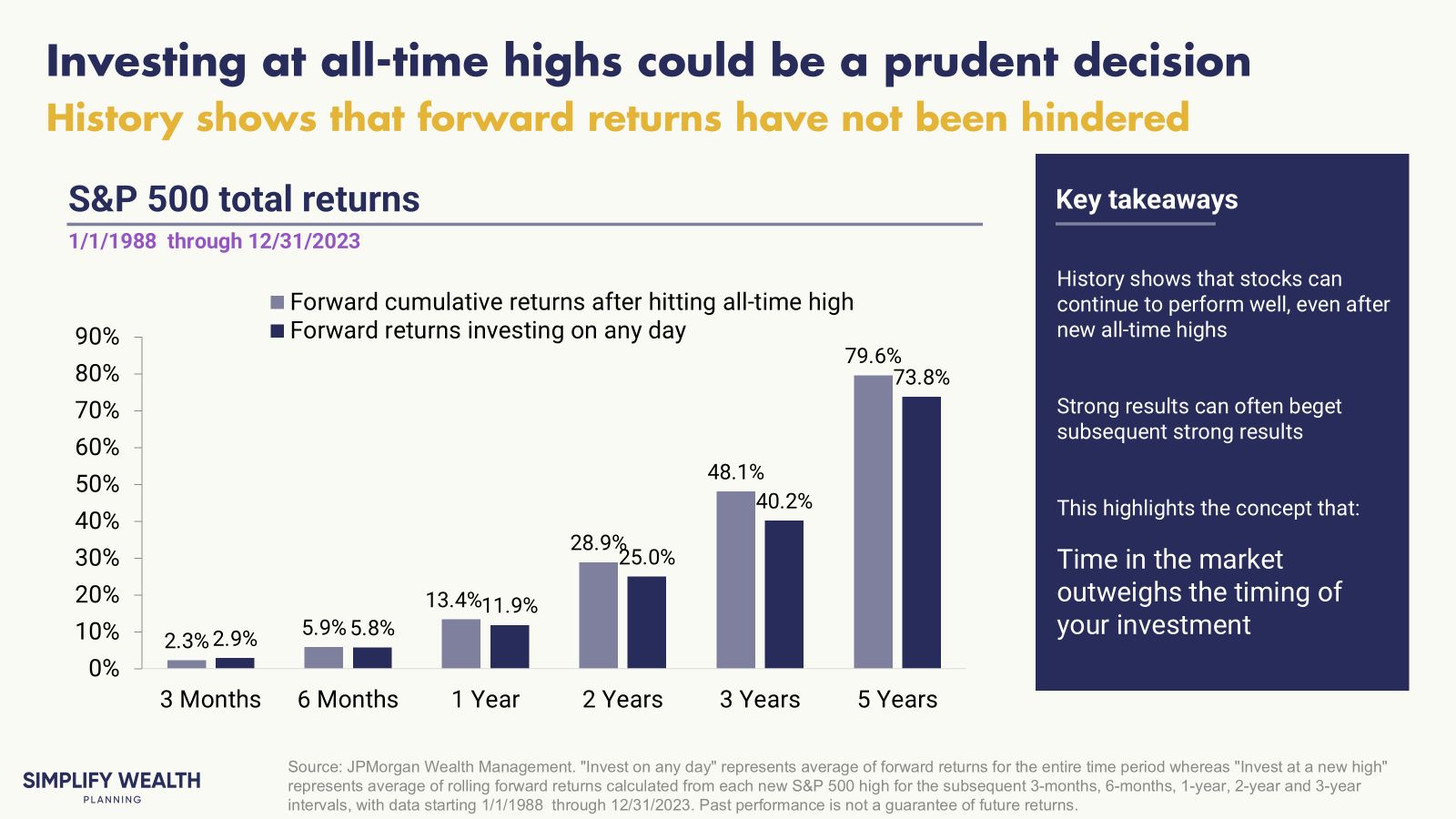

Time in the market beats timing the market.

If you lump sum at an all-time high, history shows forward returns are still positive. The S&P 500 spends a surprising amount of time near highs because new highs are built into how the system works (i.e., inflation)

The cost of waiting is cash drag. Every month you sit in cash while DCA-ing, your money misses compounding.

The Case for Dollar-Cost Averaging: Winning the Mental Game

The math says lump sum, but psychology says DCA.

Losses hurt more than gains feel good. This is a well-known behavioral bias (loss aversion). A 20% drop right after investing is the kind of pain that sticks and DCA helps you sidestep an emotional blow.

By investing systematically, you remove decision-making. No debating when to “get in.” No temptation to wait for a dip. You just follow the plan.

And in downturns, DCA makes volatility your friend. You buy more shares when prices fall, fewer when prices rise. That builds discipline and lowers your average entry price.

FAQ

What if the market is at an all-time high?

Waiting for a dip is market timing. Data shows investing at highs has still led to positive returns over time.

How long should I spread out DCA?

Six to twelve months is common. It balances the risk of a crash against the cost of sitting in cash.

Does it matter if it’s a cash bonus vs. stock sale?

No, the decision framework is the same. With stock sale proceeds, you’ve already taken the biggest step by diversifying out of company stock. The next step is a disciplined reinvestment plan.

Your Next Steps

Define the job of the money. Is this for retirement in 25 years, or a down payment in 2 years? Time horizon determines what you should be investing in.

Run the regret test. Which would sting more: investing a lump sum before a crash, or DCA-ing while the market rallies 20% and most of your money is sitting in cash? Your gut reaction will give you insight into your risk tolerance.

Use a hybrid approach. Put 25–50% in now. Dollar-cost average the rest. Capture upside while protecting against regret.

Automate the plan. Set recurring transfers so discipline is the default.

Meme of the Week

From Paralysis to Plan

The “best” strategy isn’t just about math. It’s about sticking with a plan through thick and thin.

If you feel stuck, let’s build a strategy that matches both your financial goals and your peace of mind. Schedule a call today.

This newsletter is for educational purposes only and should not be taken as individual advice

Simplify Wealth Planning

Fast-Tracking Work Optional For Employees Earning Company Stock | Turn Your Stock Comp Into Wealth, Cut Taxes & Live Life Your Way | Flat Fees Starting at $7,000

Marcel Miu, CFA and CFP®, is the Founder and Lead Wealth Planner at Simplify Wealth Planning. Simplify Wealth Planning is dedicated to helping employees earning company stock master their money and achieve their financial goals.

Rate Today's Edition:Your feedback helps us improve. Let us know what you think! |

Disclosures

Simplify Wealth Planning, LLC (“SWP”) is a registered investment adviser in Texas and in other jurisdictions where exempt; registration does not imply a certain level of skill or training.

If this e-mail refers to any client scenario, case study, projection or other illustrative figure: such examples are hypothetical and based on composite client situations. Results are for informational purposes only, are not guarantees of future outcomes, and rely on assumptions specific to the scenario (e.g., age, time horizon, tax rate, portfolio allocation). Full methodology, risks and limitations are available upon request.

Past performance is not indicative of future results. This message should not be construed as individualized investment, tax or legal advice, and all information is provided “as-is,” without warranty.