- Wealth Made Simple

- Posts

- The $40k RSU Mistake

The $40k RSU Mistake

Why the IRS just ambushed you and how to fix your system

Marcel Miu, CFA, CFP

April 19, 2026

The April 15th hangover

At some point in the last year, a smoke alarm in your house started chirping. Not a real alarm, just the low-battery chirp. Every 47 seconds. You told yourself you would deal with it. But instead, you just adapted to it. At 2am on a Tuesday, when the chirp finally woke you up for the fourth night in a row, you weren’t dealing with a battery problem anymore. You were dealing with the cost of postponing a battery problem.

RSU underwithholding works the same way. There’s a signal early in the year (your pay stub, your withholding rate, the supplemental wage cap at 22%) that tells you the math is not going to work out. Most people ignore it. Tax day is when the chirping stops and the real alarm goes off.

Why Your Company Is Under-Withholding On Your RSUs

When your equity vests, the value of those shares is taxed as ordinary income. The IRS treats those shares the same as cash deposited into your checking account. The problem isn't how the income is classified or taxed. The problem is how it’s withheld. Employers typically use the IRS default supplemental wage withholding rate of 22% for federal taxes on equity compensation up to one million dollars.

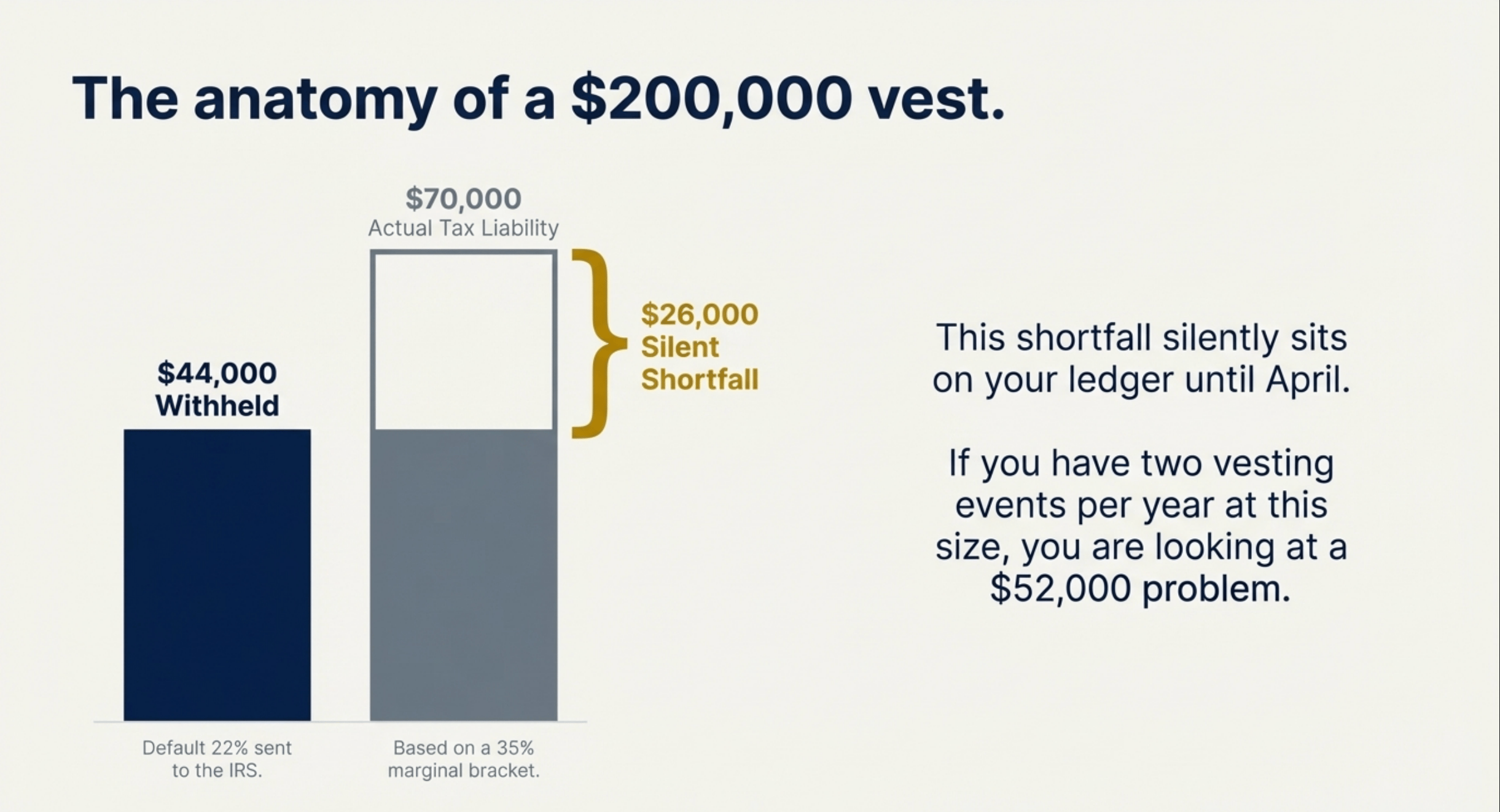

If your household income pushes you into the 32% or 35% marginal tax bracket, that default 22% withholding rate creates a massive structural gap. Let me show you the math on a $200,000 vest event:

Your company sends $44,000 to the IRS on your behalf.

You actually owe $70,000 based on a 35% marginal bracket.

That leaves a $26,000 shortfall sitting on your ledger until April.

For illustrative purposes only. Assumes a hypothetical 35% marginal tax bracket. Actual tax liabilities will vary based on individual financial circumstances and applicable state taxes.

Again, supplemental income (like RSU vests) is withheld at a flat 22% rate for the vast majority of people. This system is entirely detached from what you elect on your W-4 for your regular salary. You could ask for extra withholding on your base pay, but the payroll system will still use the flat 22% rate on your equity vest (some companies have tried to fix this, but it’s still widely done this way).

The IRS treats the two income streams differently for withholding purposes, which creates the trap. The company is following the law, but the law isn't designed to protect your personal cash flow.

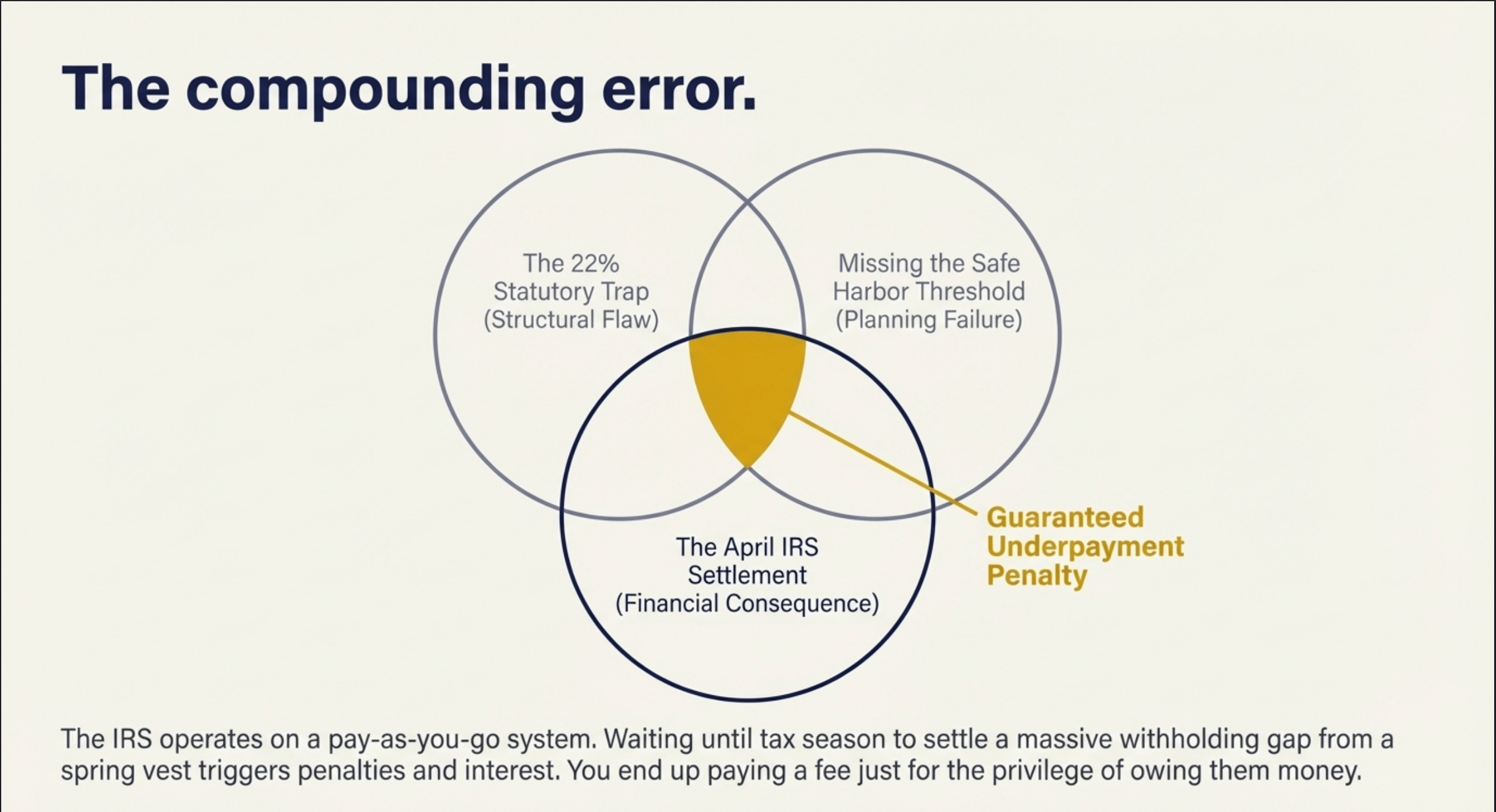

The Underpayment Penalty And Safe Harbor Rules

The IRS operates on a pay-as-you-go system. They want their money as you earn it throughout the year. Depending on your specific tax situation, waiting until tax season to settle a massive withholding gap, from a vest that happened in May of the previous year, can trigger underpayment penalties and interest.

Underpayment penalties depend on individual tax situations and safe harbor exemptions. This is an educational illustration, not a guarantee of an IRS penalty assessment.

You end up paying a fee just for the privilege of owing them money. This is an unforced error that drags down your overall wealth-building efficiency.

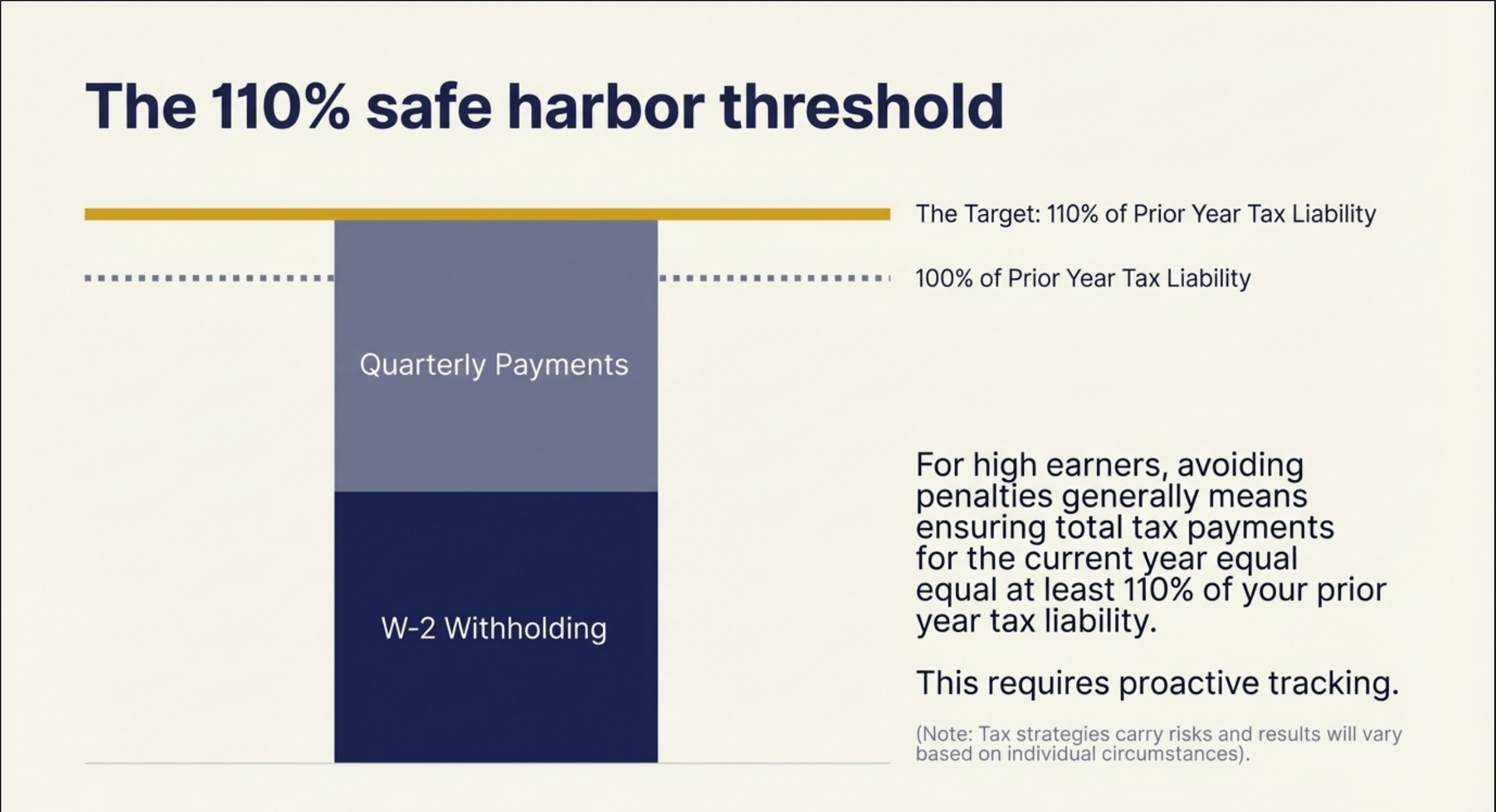

A fix for this is by utilizing safe harbor rules to help avoid these penalties. For high earners, this generally means ensuring your total tax payments for the current year equal at least 110% of your prior year tax liability.

Safe harbor rules are subject to change, and eligibility may vary based on your Modified Adjusted Gross Income (MAGI). Consult a tax advisor to determine your specific safe harbor requirements.

Meeting this threshold requires proactive planning and tracking. You have to look at your prior tax return, calculate the 110% figure, and ensure your combined W-2 withholding and quarterly payments hit that mark by the end of the year.

Some employers allow you to adjust your supplemental withholding rate directly in your equity portal. This is the cleanest fix. If yours doesn't offer this feature, you have to bridge the gap manually. You need a system to track the liability as it accrues, so you don't accidentally spend the tax money. The worst possible outcome is holding the vested shares, watching the stock price drop 30%, and still owing taxes based on the higher value at the vest date. You could be forced to sell more shares at a lower price just to cover the tax bill.

*Please remember that tax strategies carry risks and results will vary based on individual circumstances.

FAQs About RSU Taxes

Why can't my company just withhold my actual tax rate automatically based on my salary?

Payroll systems aren't designed to cross-reference your entire financial life. They don't know about your spouse's income, your outside investments, or your deductions. They follow the statutory supplemental rate to stay compliant with baseline IRS rules. Designing a system to perfectly calculate every employee's exact marginal rate in real time would be an administrative nightmare for the company.

If I sell my shares immediately on the vest date, do I avoid this tax gap?

Selling immediately is a strategy designed to help mitigate investment risk. It’s designed to help protect you from the stock price dropping before you pay the tax bill. However, it doesn't change the income tax calculation on the vest itself. You still owe ordinary income tax on the total value of the shares when they vest, and the 22% withholding problem remains. Selling just gives you the cash liquidity to pay the resulting tax bill. But you still actually need to make the payment.

Do state taxes have a supplemental withholding rate, too?

Yes. Many states mandate a specific supplemental withholding rate for equity compensation. California uses a much higher supplemental rate for stock options and RSUs than most other states. You need to verify your state-specific rules. The federal gap is usually the largest piece of the puzzle, but a state withholding gap can add thousands of dollars to your surprise April bill.

What happens if my vest pushes me into the highest federal bracket?

Statutory withholding limits are based on current federal tax code and are subject to legislative changes. For educational purposes only.

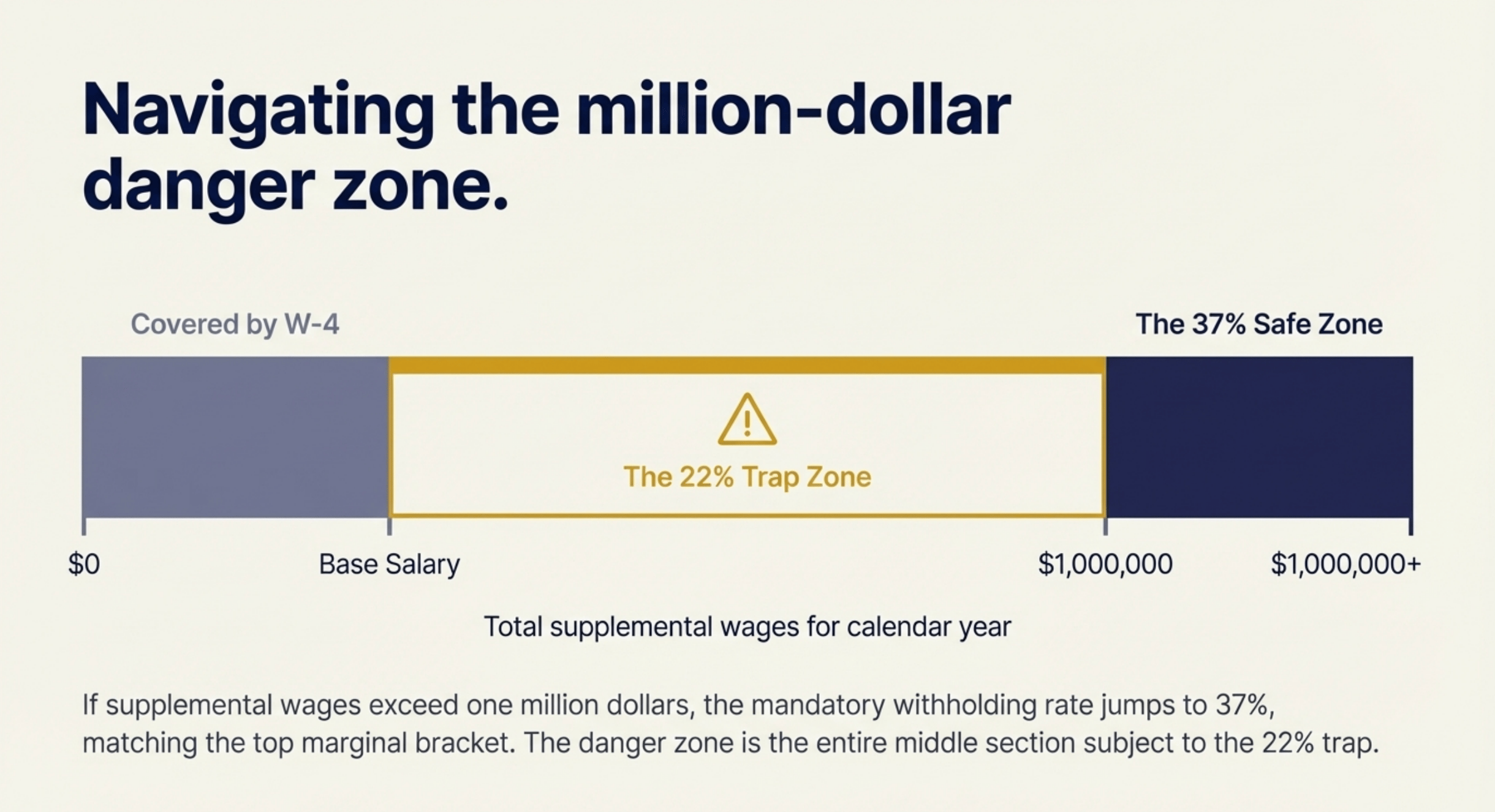

If your supplemental wages (e.g., RSU vests) exceed one million dollars during the calendar year, the mandatory federal withholding rate jumps to 37%. This actually solves the under-withholding problem for those specific dollars because the withholding rate matches the top marginal tax bracket. The danger zone is the income between your base salary and that one-million-dollar threshold. That entire middle section is subject to the 22% trap.

How To Plug The Gap

Locate your pay stub from the vest date to verify exactly what percentage was withheld.

Compare that withheld percentage against your projected marginal tax bracket for the current year to calculate your personal gap.

Check with your human resources department to see if your plan allows you to elect a higher custom withholding percentage for future vestings.

Set aside cash from your net shares to make a quarterly estimated tax payment if your employer doesn't allow custom withholding elections.

Consider adjusting the W-4 on your base salary to withhold extra dollars each pay period to cover the anticipated shortfall from your equity compensation.

Meme of the Week

Stop Tipping The IRS In Penalties

Relying on the default 22% supplemental withholding rate on your RSUs is a fast track to an unnecessary April tax shock. You’ll often end up paying underpayment penalties simply because you trusted the default system to handle the math for you. Tax efficiency isn't guaranteed, and you have to take control of the calculations to seek better outcomes.

You can keep letting the IRS hit you with surprise bills and underpayment penalties every spring, or you can take steps to address it. If you think this a department you need help in, schedule an introductory call today to learn more about our approach and determine if our services are a good fit for your family.

This newsletter is for educational purposes only and should not be taken as individual advice

Simplify Wealth Planning

Fast-Tracking Work Optional For Employees Earning Company Stock | Turn Your Stock Comp Into Wealth, Cut Taxes & Live Life Your Way | Flat Fees Starting at $8,000

Marcel Miu, CFA and CFP®, is the Founder and Lead Wealth Planner at Simplify Wealth Planning. Simplify Wealth Planning is dedicated to helping employees earning company stock master their money and achieve their financial goals.

Rate Today's Edition:Your feedback helps us improve. Let us know what you think! |

Disclosures

Simplify Wealth Planning, LLC (“SWP”) is a registered investment adviser in Texas and in other jurisdictions where exempt; registration does not imply a certain level of skill or training.

If this blog refers to any client scenario, case study, projection, or other illustrative figure: such examples are hypothetical and based on composite client situations. Results are for informational purposes only, are not guarantees of future outcomes, and rely on assumptions specific to the scenario (e.g., age, time horizon, tax rate, portfolio allocation). Full methodology, risks, and limitations are available upon request.

Past performance is not indicative of future results. This message should not be construed as individualized investment, tax, or legal advice, and all information is provided “as-is,” without warranty.

The material and discussions are for informational purposes only. These do not constitute investment advice and are not intended as an endorsement for any specific investment.

The information presented in this blog is the opinion of Simplify Wealth Planning and does not reflect the view of any other person or entity. The information provided is believed to be from reliable sources, but no liability is accepted for any inaccuracies.

We recommend consulting with your independent legal, tax, and financial advisors before making any decisions based on the information from this blog or any of the resources we provide herewithin (models, etc).