- Wealth Made Simple

- Posts

- The $66k state tax mistake

The $66k state tax mistake

High-tax states do not care where you live when your stock vests.

Marcel Miu, CFA, CFP

May 10, 2026

The "I'm Free!" Tax Illusion

Unpacking after a cross-country move is humbling. You always find that one box of tangled and obsolete charging cables. Leaving them behind was the plan. Somehow, the movers still transported them across three state lines. Moving your equity compensation feels the same. You think you left the high-tax state in the rearview mirror, and the lack of state income tax feels great right away. Reality eventually hits: your old state tax liability followed you right into your new house.

Whether you hold standard RSUs at a corporate giant or double-trigger RSUs waiting for a liquidity event, high-tax states have a long memory. The tax bill does not magically disappear when you cross the border.

How High-Tax States Track Down Your Equity

You moved to a no-tax state like Texas or Florida. Why is California or New York still taxing my stock vests?

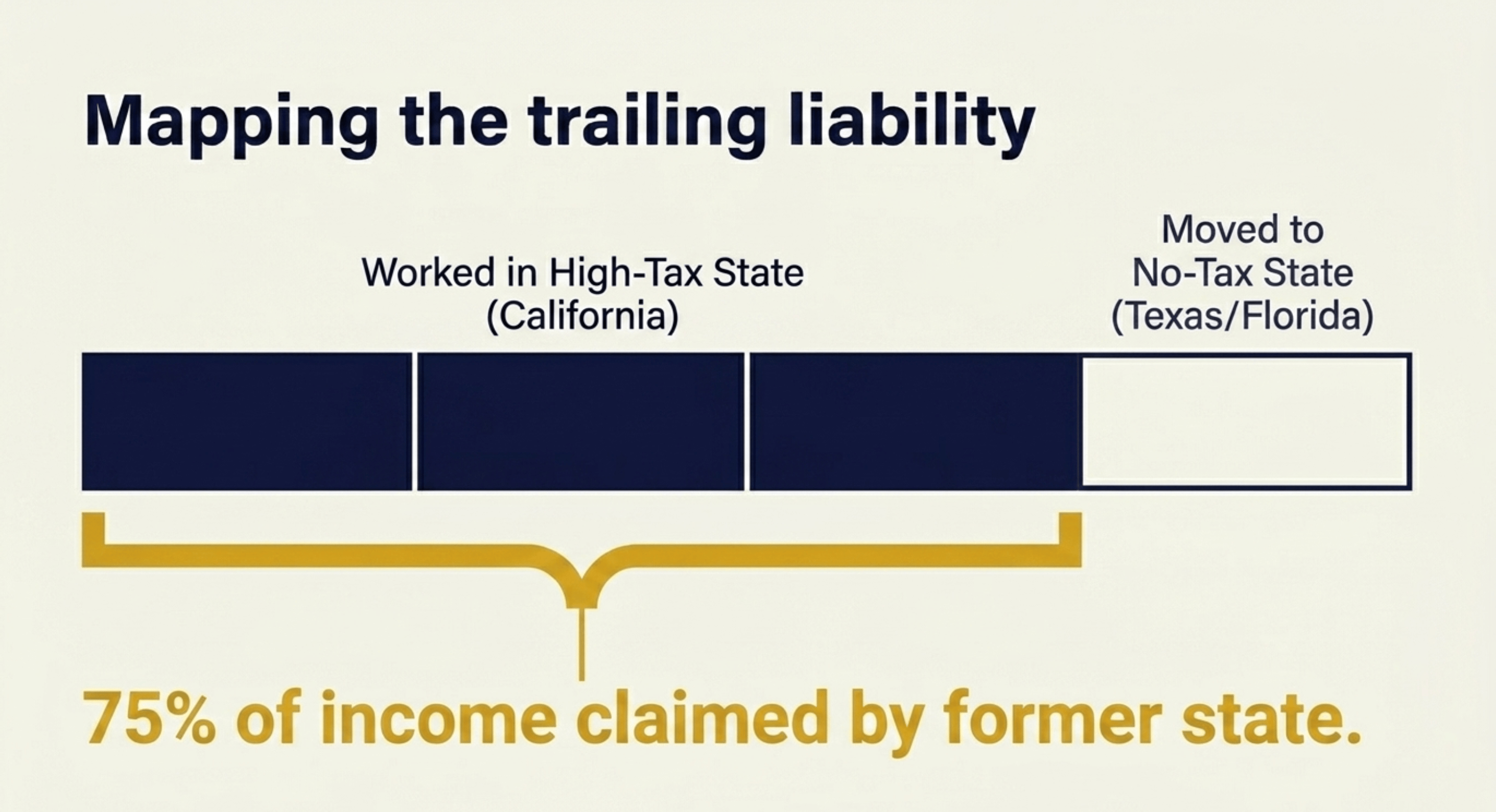

The answer comes down to the workday allocation formula. High-tax states do not care where you live when your stock vests. They care where you lived when you earned it. If you worked in a state like California for three years of a four-year vesting schedule, California claims 75% of that income. Let me explain.

Hypothetical scenario for illustrative purposes. Actual workday allocation formulas vary by jurisdiction.

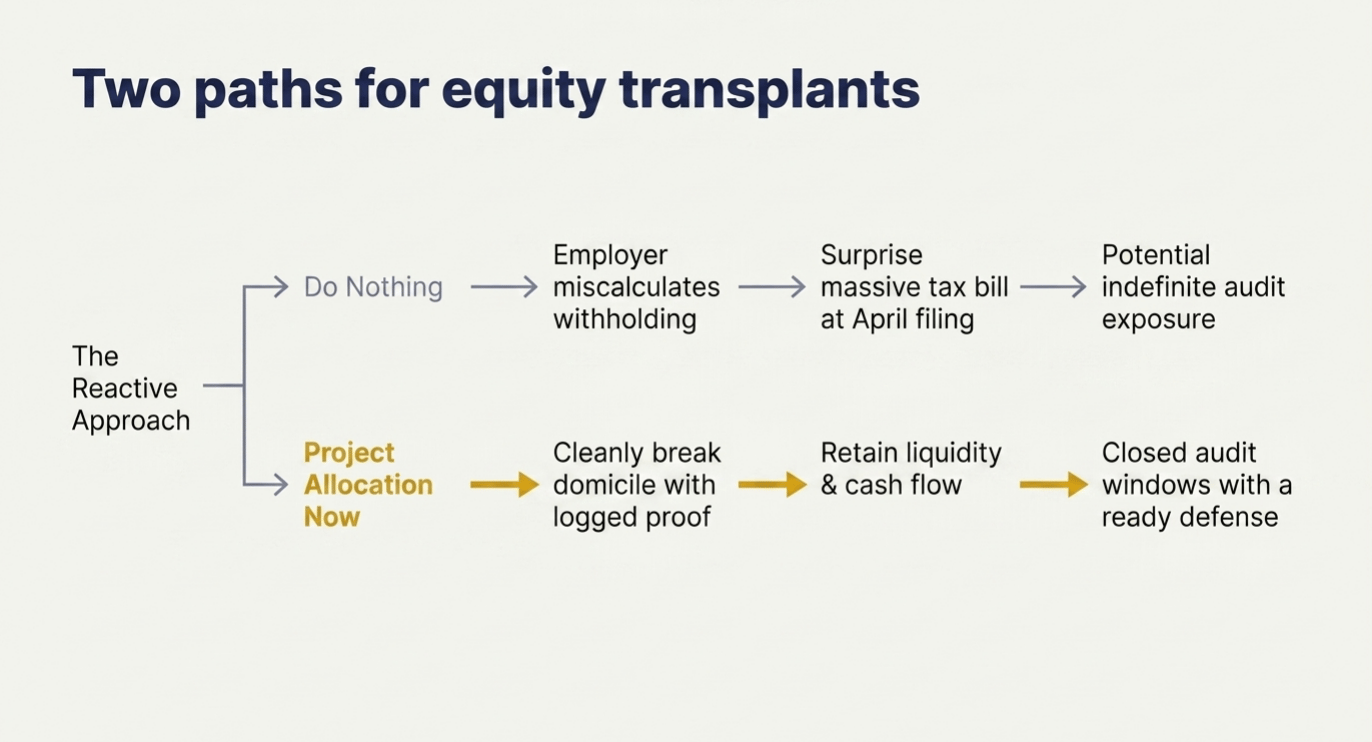

State tax laws are designed to capture revenue from equity generated within their borders. Many employees assume their payroll system handles this automatically, but it rarely does. When you move, your employer might stop withholding state tax entirely from your pay for your old state. You receive the shares and think you are in the clear. Come April, your tax preparer runs the workday allocation formula, and suddenly you have a massive tax bill and potential underpayment penalties.

Here’s the math. Let’s say you have a $500,000 vest event coming up. If California applies its top 13.3% rate based on your historical workday allocation, you could owe $66,000 to a state you don’t live in anymore.

And the California Franchise Tax Board is notoriously ruthless. They look at forensic data to prove where you were actually working. We are talking about cell phone records, credit card swipes, and flight logs. They will track you down. Ignoring the trailing liability is not a viable strategy.

The Double-Trigger Trap

If you work for a private company with double-trigger RSUs, the workday allocation formula presents a severe relocation risk.

Hypothetical illustration. Equity compensation is subject to severe investment and tax risks, including the potential for loss of principal.

Say you worked in a high-tax state for years, and then you moved to a no-tax state. Then the IPO hits. All those years of built-up equity instantly become taxable income. The high-tax state uses the allocation formula to take a massive tax bite out of your liquidity event. And the massive tax bill arrives all at once.

FAQ About State Tax Audits

If I just use a friend's address in Texas while I finish working in California, am I safe?

Absolutely not. Auditors pull mobile device location histories to confirm where you physically sat while working. Faking a residency leaves you exposed to audits and severe penalties. State tax boards look for the true economic center of your life.

Do stock options follow the same workday allocation rules as RSUs?

Yes. Non-qualified stock options and Incentive Stock Options are also subject to allocation. The math is based on the grant-to-vesting period or grant-to-exercise period. The exact calculation depends on the specific state regulations and the type of option.

How long does a high-tax state have the right to audit my residency status after I move?

The statute of limitations varies by state. In California, the FTB generally has four years from the date you file your return to initiate an audit. If you never file a non-resident return reporting the trailing equity income, the clock never starts. The exposure remains open indefinitely.

Defending Your Domicile

Establishing a new domicile requires more than just signing a lease. You need to prove a permanent break from your old state.

Update all physical and digital ties immediately. This includes your driver's license, voter registration, and vehicle registration.

Pull a year-to-date travel and work-location log. You need to calculate your exact ratio of days worked in the high-tax state versus the new state.

Keep your boarding passes and moving company receipts on file. The burden of proof is on you if audited.

Review your unvested equity schedule. Project the exact trailing tax liability you could face over the next few years.

Sever local memberships. Cancel the old gym, the local country club, and any professional affiliations tied to your former home.

Meme of the Week

Stop Guessing on Your Trailing Tax Bill

For educational purposes only.

Moving to a no-tax state is often a smart financial move. But until your previously granted equity fully vests, you are still potentially on the hook for the trailing tax bill. Planning helps prevent a cash flow crisis when tax season arrives.

Schedule an introductory call today to learn how our planning process seeks to bring clarity to complex equity transitions and help you build a solid defense plan.

This newsletter is for educational purposes only and should not be taken as individual advice

Simplify Wealth Planning

Fast-Tracking Work Optional For Employees Earning Company Stock | Turn Your Stock Comp Into Wealth, Cut Taxes & Live Life Your Way | Flat Fees Starting at $8,000

Marcel Miu, CFA and CFP®, is the Founder and Lead Wealth Planner at Simplify Wealth Planning. Simplify Wealth Planning is dedicated to helping employees earning company stock master their money and achieve their financial goals.

Rate Today's Edition:Your feedback helps us improve. Let us know what you think! |

Disclosures

Simplify Wealth Planning, LLC (“SWP”) is a registered investment adviser in Texas and in other jurisdictions where exempt; registration does not imply a certain level of skill or training.

If this newsletter refers to any client scenario, case study, projection or other illustrative figure: such examples are hypothetical and based on composite client situations. Results are for informational purposes only, are not guarantees of future outcomes, and rely on assumptions specific to the scenario (e.g., age, time horizon, tax rate, portfolio allocation). Full methodology, risks and limitations are available upon request.

Past performance is not indicative of future results. This message should not be construed as individualized investment, tax or legal advice, and all information is provided “as-is,” without warranty.

The material and discussions are for informational purposes only. These do not constitute investment advice and is not intended as an endorsement for any specific investment.

The information presented in this blog is the opinion of Simplify Wealth Planning and does not reflect the view of any other person or entity. The information provided is believed to be from reliable sources, but no liability is accepted for any inaccuracies.

We recommend consulting with your independent legal, tax, and financial advisors before making any decisions based on the information from this blog or any of the resources we provide herewithin (models, etc).