- Wealth Made Simple

- Posts

- I asked a client to consider selling their stock and they panicked

I asked a client to consider selling their stock and they panicked

You might be making a huge mistake with your vested shares.

Marcel Miu, CFA, CFP

March 22, 2026

The trap of the house money illusion

Tech earnings season wrapped up. My inbox was littered with questions from clients looking at their company stock positions.

They stare at their huge equity balances and feel euphoric yet paralyzed.

They want a clear financial plan to give them a sense of direction and want to know they are making the right choice for their family.

When the numbers get large, a dangerous psychological trap kicks in. You fall for the house money illusion. You feel like you’re playing with casino chips instead of your own wealth.

This leads to decisions you would never make with cash.

Clients often get frustrated about the big tax bills they have to pay if they sell their vested shares. They then drain their cash savings to hold onto the company stock. And give up their safety net because they can’t bear to part with the shares.

This represents a classic case of mental conflict and stems from a powerful psychological bias. I have a few clients who have been especially stressed by this recently, with all the turmoil we’ve seen across the tech sector. Stressed out, they imagine the financial devastation of a market crash. They fear having to delay retirement by a decade just because they held on too long.

I suggested we review their concentration risk and consider outlining a selling strategy. They told me they couldn't sell because it might bounce back.

Human psychology clashes with financial reality in these moments.

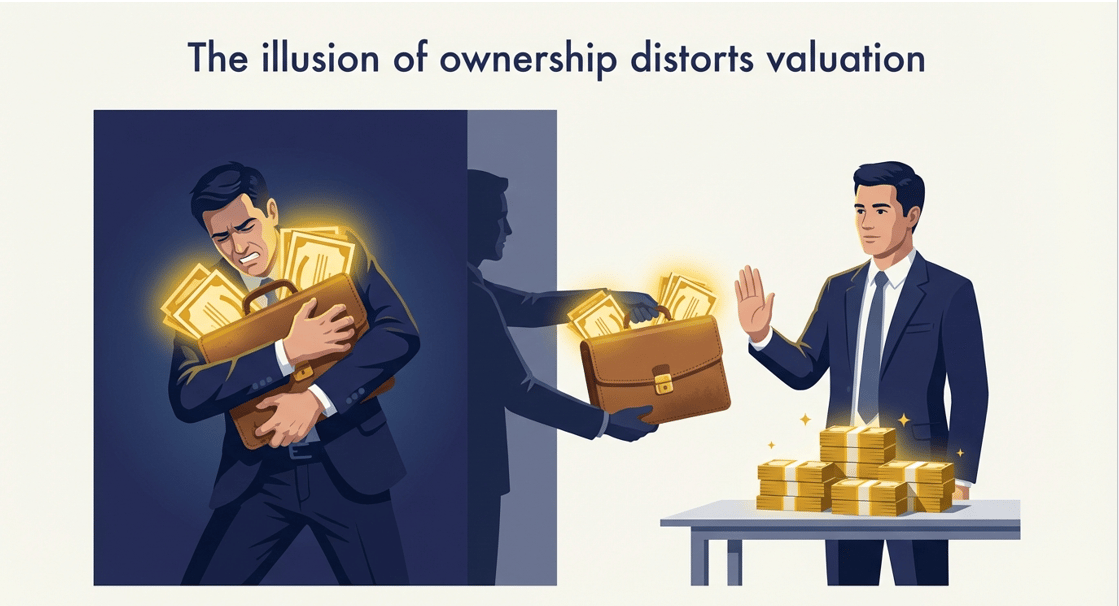

Why do you refuse to sell your shares?

Imagine someone handed you one million dollars in cash today. You'd likely refuse to use it all to buy a huge block of your company stock.

Every professional would agree with this. They admit it carries way too much risk. Yet employees refuse to sell their vested equity. You're mathematically making that same decision every single vesting day. You crave confidence, peace of mind, and want to reduce anxiety. Holding concentrated stock often does the exact opposite.

This irrational behavior stems from the endowment effect. This behavioral finance bias means humans overvalue things they own.

But another bias conflicts with that: we're hardwired for loss aversion. The pain of losing far exceeds the joy of winning.

You feel the sting of a ten-thousand-dollar loss much more intensely than the thrill of a ten-thousand-dollar gain. You fear selling, watching the stock go up, and missing out more than you fear watching your net worth drop.

Doing well with money has little to do with how smart you are. It has a lot to do with how you behave. You want to simplify complex financial decisions to reduce your mental burden. Understanding this bias helps you take back control.

Note that all investments carry risk, and behavioral awareness doesn't guarantee a profit or protect against loss.

This slide is for educational purposes only and illustrates a behavioral finance concept. It is not intended as investment advice or a recommendation to buy or sell any security. Individual investment decisions should be based on a client’s specific objectives, risk tolerance, and financial situation.

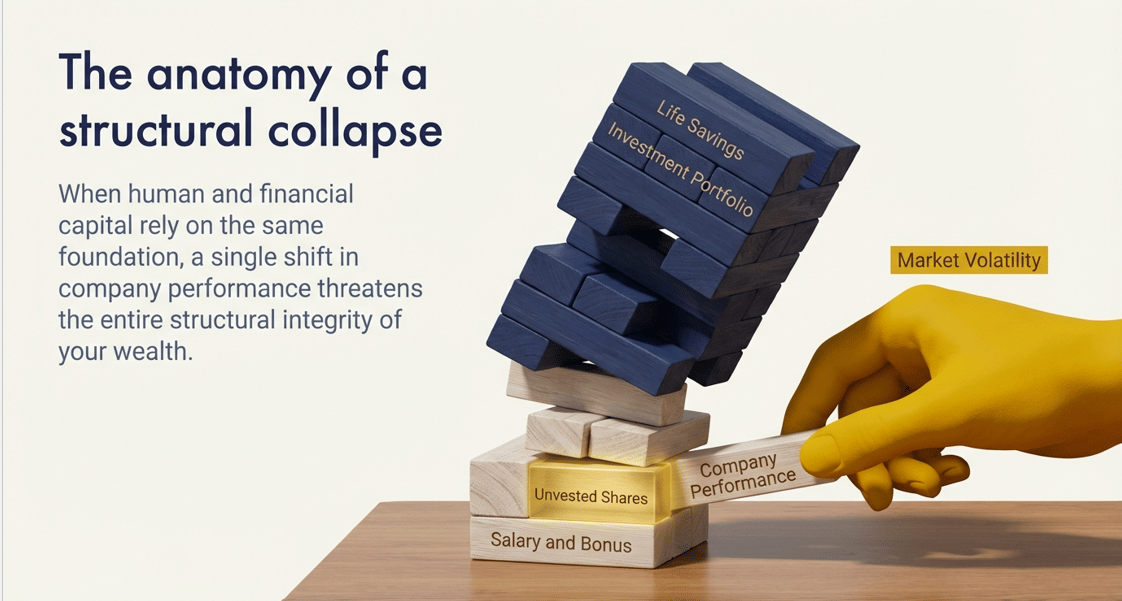

The danger of the double bet

You might think it makes sense to bet on the horse you ride because you know your company best. This approach can create a significant single point of failure.

You already tie your ability to earn money to your employer. Your salary, your bonuses, and your unvested future grants depend on them. You also rely on your company for your health insurance.

A market crash puts your entire financial stability at risk.

You need to hedge that exposure. The prospect of losing your job sends waves of panic through you. And you double down on that same exposure when you invest all your savings back into the same company.

This illustration is for educational purposes only and is intended to demonstrate concentration and correlation risk. It is not a recommendation to buy or sell any security or to take any specific investment action. All investments involve risk, including possible loss of principal.

FAQ

Q. People often ask if they should sell their shares the day they vest?

Many financial planners suggest considering an immediate sale. Shares become taxable as ordinary income when they vest. You've already paid income tax on the vesting of those shares. If you hold them, it's the same thing as taking your cash paycheck and buying your company stock on the open market.

Taxes are often the biggest hurdle preventing professionals from diversifying. Before you sell your vested shares, you'll want to review our guide on navigating tax implications for restricted stock units in high-income tax brackets to ensure you don't face an April surprise.

Q. What happens if the stock goes up right after I sell?

You don't need to capture every penny of upside to achieve financial independence. You need to avoid a catastrophic loss that resets your timeline. You want to build and grow your wealth for security and legacy. A massive loss prevents that.

Q. How much company stock is too much?

A single stock making up more than twenty percent of your total net worth means you likely have a concentrated stock problem. This requires risk management. If you fear failing to achieve your financial goals, limiting your single stock exposure helps protect those dreams.

Your Next Steps

Here are steps you can take right now to remove the emotion from your equity compensation.

Take the blank slate test. Log in to your brokerage portal today. Look at the total cash value of your vested company stock. Ask yourself out loud if you'd use it all to buy this stock if it were sitting in your checking account right now. Reevaluate your holding strategy if the answer is no.

Automate the exit. Stop trying to time the market. Set up a schedule to sell a specific number of shares every quarter. Automation helps mitigate the endowment effect.

Cap your exposure. Pick a hard percentage limit for your net worth. Trim the stock back down to that number if it rallies and pushes your allocation higher.

Shift your mindset. Write this on a sticky note and put it on your monitor. Vested shares are cash bonuses paid in stock. Treat them as cash the moment they hit your account. If you desire efficient processes that save time and reduce hassle, this mindset shift simplifies your financial life.

If you're starting to realize that your portfolio has become too top-heavy with your employer's equity, you'll want to check out my deep dive on managing concentrated positions to explore specific exit strategies.

Meme of the Week

Break the handcuffs

You won the hardest part of the game by earning the equity. Don't risk your financial freedom by letting psychological biases trick you into betting it all on one horse. Remember that investing involves risk, including the possible loss of principal.

Hit reply or click here to schedule a free portfolio risk assessment if you're tired of losing sleep over the swings in your company stock. We'll build an objective and math-driven plan to manage your concentration. Let's work together to align your risk with your long-term goals.

This newsletter is for educational purposes only and should not be taken as individual advice

Simplify Wealth Planning

Fast-Tracking Work Optional For Employees Earning Company Stock | Turn Your Stock Comp Into Wealth, Cut Taxes & Live Life Your Way | Flat Fees Starting at $7,000

Marcel Miu, CFA and CFP®, is the Founder and Lead Wealth Planner at Simplify Wealth Planning. Simplify Wealth Planning is dedicated to helping employees earning company stock master their money and achieve their financial goals.

Rate Today's Edition:Your feedback helps us improve. Let us know what you think! |

Disclosures

Simplify Wealth Planning, LLC (“SWP”) is a registered investment adviser in Texas and in other jurisdictions where exempt; registration does not imply a certain level of skill or training.

If this newsletter refers to any client scenario, case study, projection, or other illustrative figure: such examples are hypothetical and based on composite client situations. Results are for informational purposes only, are not guarantees of future outcomes, and rely on assumptions specific to the scenario (e.g., age, time horizon, tax rate, portfolio allocation). Full methodology, risks, and limitations are available upon request.

Past performance is not indicative of future results. This message should not be construed as individualized investment, tax, or legal advice, and all information is provided “as-is,” without warranty.

The material and discussions are for informational purposes only. These do not constitute investment advice and are not intended as an endorsement for any specific investment.

The information presented in this blog is the opinion of Simplify Wealth Planning and does not reflect the view of any other person or entity. The information provided is believed to be from reliable sources, but no liability is accepted for any inaccuracies.

We recommend consulting with your independent legal, tax, and financial advisors before making any decisions based on the information from this blog or any of the resources we provide herewithin (models, etc).